Fine print: renters insurance agreement answer key – this phrase sets the stage for a comprehensive exploration of the intricacies hidden within renters insurance policies. Understanding these details is paramount for renters seeking to fully protect their belongings and avoid unexpected pitfalls.

Navigating the fine print of a renters insurance agreement requires a keen eye and a thorough understanding of its implications. This guide delves into the key provisions, exclusions, and limitations that renters should be aware of, empowering them to make informed decisions and maximize their coverage.

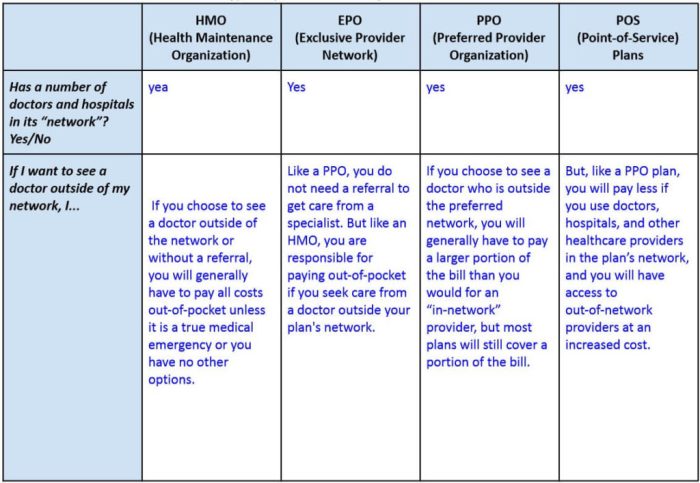

Renters Insurance Agreement Overview

A renters insurance agreement is a contract between a renter and an insurance company that provides coverage for the renter’s personal property and liability.

Typical coverage included in a renters insurance policy includes:

- Personal property coverage: This covers the renter’s belongings, such as furniture, clothing, and electronics, in the event of damage or loss due to covered perils, such as fire, theft, or vandalism.

- Liability coverage: This covers the renter’s legal responsibility for injuries or property damage caused to others.

- Additional living expenses coverage: This covers the renter’s additional living expenses, such as hotel bills or temporary housing, if the renter is unable to live in their rented property due to a covered peril.

It is important to carefully review the fine print of a renters insurance agreement to understand the specific terms and conditions of the coverage.

Identifying Key Provisions in the Fine Print: Fine Print: Renters Insurance Agreement Answer Key

![]()

Renters should pay attention to the following key provisions in the fine print of their insurance agreement:

- Covered perils:These are the events or occurrences that are covered by the insurance policy. Common covered perils include fire, theft, vandalism, and water damage.

- Exclusions:These are the events or occurrences that are not covered by the insurance policy. Common exclusions include damage caused by earthquakes, floods, and acts of war.

- Deductible:This is the amount that the renter must pay out-of-pocket before the insurance company will begin to pay for covered losses.

- Policy limits:These are the maximum amounts that the insurance company will pay for covered losses. Policy limits can vary depending on the type of coverage and the insurance company.

These provisions can significantly impact the coverage provided by the insurance policy, so it is important to understand them before purchasing renters insurance.

Understanding Exclusions and Limitations

Renters insurance agreements may include exclusions and limitations that restrict the coverage provided. Common exclusions include:

- Acts of war:Damage caused by acts of war is typically excluded from coverage.

- Earthquakes:Damage caused by earthquakes is typically excluded from coverage, unless the renter purchases an earthquake endorsement.

- Floods:Damage caused by floods is typically excluded from coverage, unless the renter purchases a flood insurance policy.

Limitations may also be included in the insurance agreement, which limit the amount of coverage provided for certain types of losses. For example, there may be a limit on the amount of coverage provided for jewelry or other valuables.

Claim Filing Procedures

Renters should follow the claim filing procedures Artikeld in the fine print of their insurance agreement. These procedures typically involve the following steps:

- Contact the insurance company:The renter should contact the insurance company as soon as possible after a covered loss occurs.

- File a claim:The renter will need to file a claim with the insurance company, which will typically involve providing documentation of the loss.

- Provide documentation:The renter will need to provide documentation of the loss, such as receipts for damaged or stolen property.

- Cooperate with the insurance company:The renter will need to cooperate with the insurance company’s investigation of the claim.

There may be deadlines or time limits associated with claim filing, so it is important to follow the procedures Artikeld in the insurance agreement.

Dispute Resolution and Legal Rights

If a renter disagrees with a claim decision, they may have the right to file a dispute with the insurance company. The dispute resolution process will vary depending on the insurance company, but it typically involves the following steps:

- File a written appeal:The renter will need to file a written appeal with the insurance company, explaining why they disagree with the claim decision.

- Review by the insurance company:The insurance company will review the renter’s appeal and make a decision on whether to uphold or overturn the claim decision.

- External review:If the renter is still not satisfied with the insurance company’s decision, they may be able to file a complaint with an external review board or the state insurance commissioner.

Renters also have certain legal rights under the terms of their insurance agreement. These rights may include the right to:

- Receive a fair and timely settlement of their claim.

- Be treated fairly and respectfully by the insurance company.

- File a complaint with the state insurance commissioner if they believe the insurance company has violated their rights.

FAQ Summary

What are the key provisions to look for in a renters insurance agreement?

Key provisions include coverage limits, deductibles, exclusions, and claim filing procedures.

How do exclusions and limitations affect coverage?

Exclusions and limitations can restrict coverage for certain types of losses or events, reducing the amount of protection provided.

What steps should renters take to file a claim?

Renters should promptly report claims to their insurance company and provide documentation to support their claim.